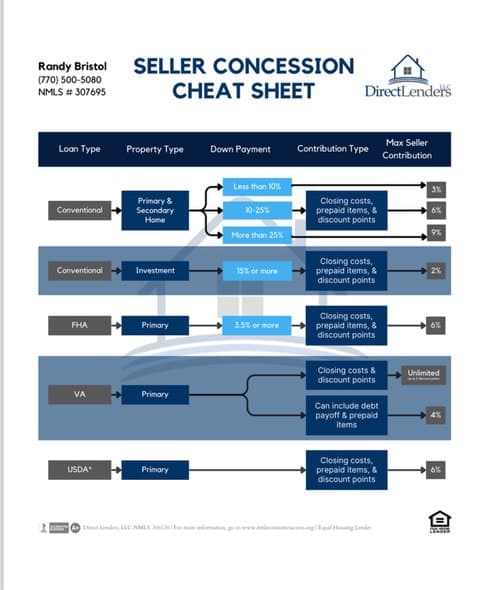

At closing, when a home sale is finalized, the closing attorney goes line by line through an accounting of all the funds. This is where the home-buyer pays their “closing costs” such as their home owners insurance premium and loan origination fees. The home-seller pays their closing costs such as prorated property taxes, and prorated home owners association dues. During negotiations, the buyer or more commonly, the seller may occasionally agree to pay some of the buyer’s closing cost fees. But, not everyone knows, when the buyer is obtaining a home mortgage loan from a lender, the lenders have limits on the amount of funds a seller may contribute. They are outlined in the chart here provided by Direct Lenders. Working with a real estate professional - like us - who knows these details will help home-buyers ensure you don’t leave “money on the table” at closing. And help ensure a smooth closing all around with no last minute scrambling to “balance” the numbers. If the seller agrees to $10,000 but the lender only allows $8,000… then that’s $2000 that goes back into the sellers pocket. P.S. As a rule of thumb, closing costs usually amount to about 3% of the purchase price of the home.