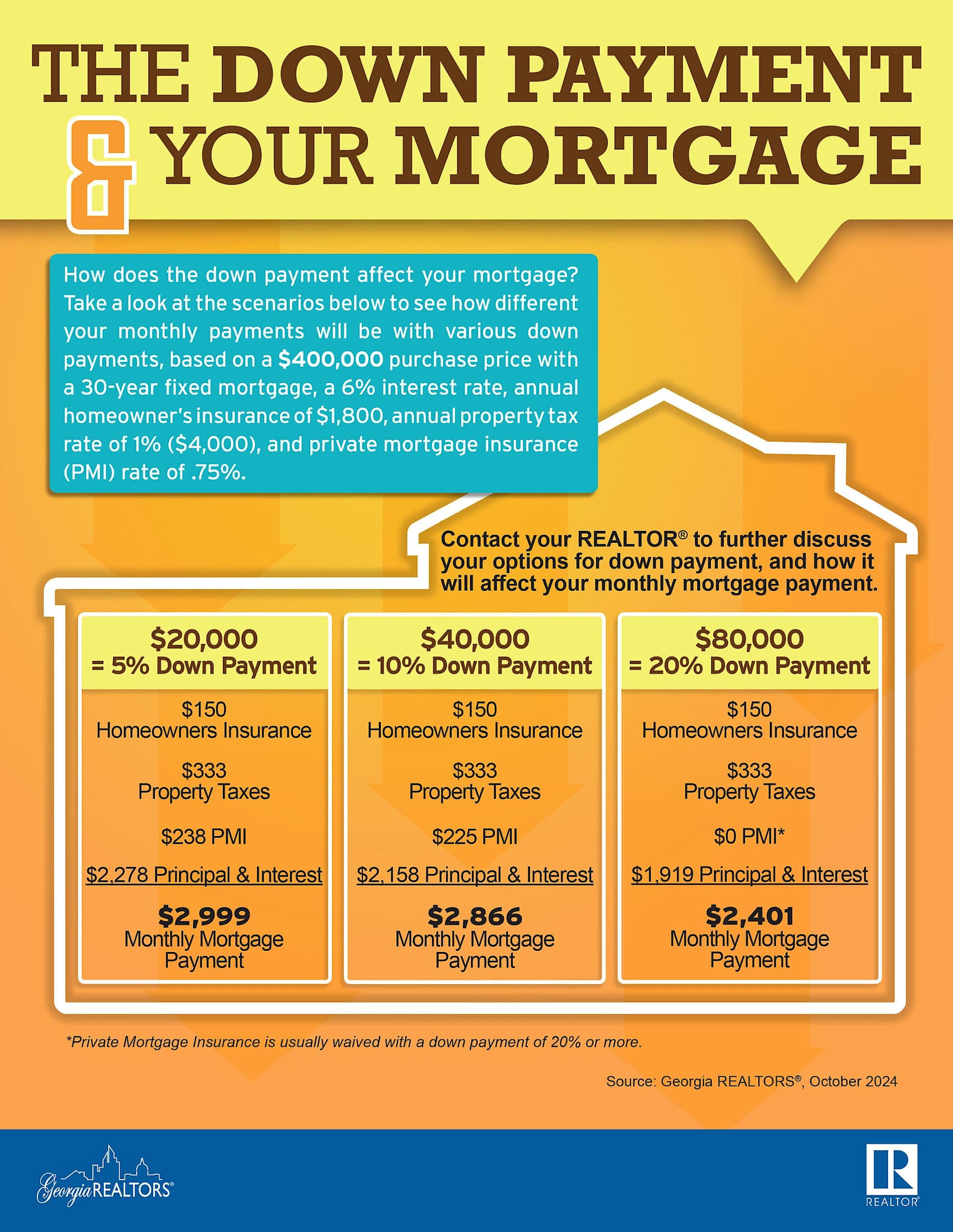

When buying a home, the amount you put down can significantly affect your monthly mortgage payments. Let’s break down how down payment amounts influence various costs, using a $400,000 home purchase as an example with a 30-year fixed mortgage, a 6% interest rate, annual homeowner’s insurance of $1,800, a 1% property tax rate, and a PMI (private mortgage insurance) rate of 0.75%.

1. 5% Down Payment ($20,000)

•PMI: $238

•Principal & Interest: $2,278

•Total Monthly Payment: $2,999

2. 10% Down Payment ($40,000)

•PMI: $225

•Principal & Interest: $2,158

•Total Monthly Payment: $2,866

3. 20% Down Payment ($80,000)

•PMI: $0 (PMI is typically waived with a 20% down payment)

•Principal & Interest: $1,919

•Total Monthly Payment: $2,401

Key Takeaways

•Lower Down Payment: While it may get you into a home sooner, it generally results in a higher monthly payment due to PMI.

•Higher Down Payment: This lowers monthly payments by reducing the loan principal and typically waives PMI, offering substantial monthly savings.

Each down payment scenario provides different financial outcomes, so assessing which fits your budget and long-term goals is essential.

Have Questions?

Your down payment decision is unique to your financial situation. Connect with a Sage and Grace REALTOR® to discuss your options and understand how to structure your down payment for your home purchase. We’re here to help you make informed choices and guide you every step of the way! At Sage and Grace Realty, we are dedicated to providing expert guidance and support through every step of the home buying and selling process. Contact us today to discuss your options and find the best approach for your real estate needs.

Source: Georgia REALTORS®, October 2024